It won’t come as a surprise to many to learn that the current state of finance in Australia is not what it once was. In fact, the Australian Bureau of Statistics (ABS) recently announced that the household saving ratio was 2.8% in the January – March 2019 quarter. In comparison, between 2008 and 2015, the household savings ratio was almost completely above 6%, with the savings rate above 8% for a fair amount of time between December 2008 and 2012.

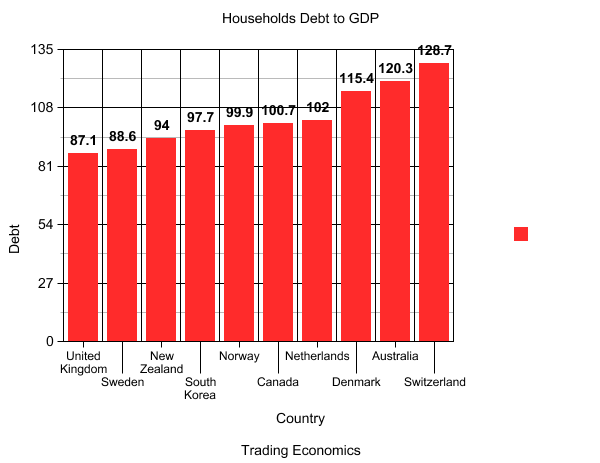

source: tradingeconomics.com

It’s likely that a lot of this decline can be attributed to servicing higher debt values. Australia ranks as having some of the worst household debt in the world. In fact, Australia ranks as having the second-highest debt in the world, after Switzerland.

So what is contributing to this startling increase? Well, in general terms, it can be put down to a mixture of overspending, higher mortgages, and the increased cost of living.

An increasing number of Australians are relying on quick, cash loans – often referred to as ‘payday loans’ – to make ends meet at a time when the cost of living is extremely high. But cash loans haven’t always had a great reputation in Australia.

So, let’s talk payday lending … what’s the story?

What is a payday loan?

Perhaps it would be best to talk about what a payday loan is first. It seems to be that the term evokes a constant state of fear – the term ‘predatory lending’ is often associated, and it is considered ‘shady’ at best. But, that could just be down to negative press and a misunderstanding of what the term actually means.

Simply put, a payday loan is a high-interest, short-term loan. Payday loans usually include small amount loans, however can also include loans borrowed over longer periods.

The term payday loan is said to relate to the need to rely on a person’s upcoming paycheck in order to secure or payback the loan. When we look at removing the fear and negativity associated with the term, it should really just be considered another word for cash loan or short term loan.

What does the Australian state of finance mean for the payday loans industry?

Payday loans have never had a great reputation here in Australia. But the fact is, they are a necessary requirement for lots of people who simply can’t meet bank lending requirements and find themselves with an immediate need for access to funds. Regulation around payday lending in Australia has been in place for some time, and regulatory bodies govern the industry to ensure that the financially vulnerable are not taken advantage of.

But that’s not to say that payday lending is for everyone. And for many of the people who take them out, payday loans are a required means to an end and do not always have a negative effect. For example, a report from Policis titled “A research study of the use and impact of payday lending in the domestic Australian market” notes that,

“The evidence does not support the view that payday borrowers tend to become trapped in a debt spiral of continually extended or renewed loans.”

So why do we see such a negative depiction of payday lending in the media?

Payday lending and the media

Media hype and the need to sell a story could be the simple answer. Lots of the negative commentary we see is not always justified. We’re told of horror stories around people who are accessing cash loans when they simply shouldn’t be. But, like all industries, there are minorities and cases where things happen that simply should have been prevented.

Does this mean that everyone should be tarred with the same brush? Just because one travel agent didn’t do a good job, does this mean that all travel agents are bad? We could apply the same logic to how the media treats the payday lending industry.

Risk management by payday lenders

In addition to the somewhat fear mongering articles we read around payday lending, we also see articles that seem to lack the facts. The truth is, application assessment technology is in place – for the most part – to prevent situations occurring that result in a blatantly unsuitable person receiving funds from a payday lending source. Responsible lending and the bodies that monitor this are key to the operation of many payday lenders.

Those who take out payday loans

When we look at the majority of people who are benefiting from these types of loans, we know that they suffer from financial exclusion. These are people who don’t have any other option.

It’s important that these people have access to loans and protection – which is why cash loan companies like Nimble exist. We realise how important a credit score is, but we also acknowledge that your financial footprint with regards to your income vs outgoing and how you manage money is important too. In some cases, this is more relevant than a mark against your credit score many years ago.

Payday loan alternatives

Looking at how the ‘buy now, pay later’ space has evolved, we knew that the positives were evident from the start. Easy, accessible lending with no fuss. But, we saw a key component missing – customisation. You can’t alter the dates of your payment reschedule with this type of lending, or the length of time in which payment is made, and we know that this type of customisation is very important to our customers.

Nimble has been effectively providing payday loans for many years. We offer our customers all the ease of buy now, pay later, with the benefit of a customised repayment plan for our small and medium cash loans.

And now, in an exciting new path, we’re moving into a new space that focuses on providing a greater number of medium-sized loans, using smart technology that reads your bank statements and groups your income and expenses to allow us to make an informed decision on your suitability. With Nimble it’s never just about your credit score – it’s about living.

What’s next for the payday loans industry?

We know that Nimble are taking leaps and bounds in the ‘payday loan space’, and now we’re moving into providing more fast and easy lending solutions at a larger scale. Saying goodbye to payday lending is a huge step for us, but we intend to continue to operate with speed and agility – putting our customers at the heart of all we do.

We predict that the coming years will continue to see a growing need for fast cash loans, and that regulations will continue to tighten to ensure the space operates in a fair and legitimate way. We’re committed to these regulation changes as a responsible lender, while still ensuring we service the people who need us most.

To find out more about Nimble, and to compare our financial products, visit our website here.

Disclaimer: Please note this content is provided as general information only and does not take into account your objectives, financial situations or needs. For advice tailored to your financial situation, it is advised that you seek guidance from an accountant or financial advisor. The above post refers to application software (“App, Apps”) that is not affiliated or associated with Nimble. We do not have any control or responsibility over the content of the Apps. Use of the Apps may be subject to further terms and conditions imposed by the App provider, the owner of the mobile operating system and/or other related parties. The above links belong to a variety of websites and not Nimble, so clicking on, and using them, will take you away from Nimble’s website meaning we’ve got no control or responsibility over the content. Nimble does not endorse and is not affiliated or associated in any way whatsoever to the businesses named in this blog post. The information contained in this article is correct at the date of publication.

Popular Posts

12 Ways to Make Money Without Having a Traditional Job

August 19, 2019

The complete home maintenance budget guide and how a home renovation loan could help

April 30, 2019

Budget Planning for Students: The University Student Budgeting Guide

June 5, 2019

Our Before-and-After Photo Competition

December 14, 2021